You've googled retirement calculators, punched in numbers, and felt absolutely nothing useful come out of it. Expat life is genuinely more complicated than most people think, and the standard tools weren't built for you: multiple countries, multiple currencies, no single system that holds it all together. To add on to that frustration, not knowing if you are on track is its own kind of stress. This guide will give you a clear framework for taking the next steps toward retirement.

Key Takeaway

Standard retirement tools weren’t built for expat life. Here’s what you actually need to know:

- Your retirement income number is probably higher than you think, and harder to calculate when you’re spending in one currency and saving in another.

- Pension pots from previous countries don’t manage themselves. Most expats have at least one sitting in a default fund, unreviewed, underperforming.

- Tax residency, domicile, and cross-border treaties affect how your retirement income is taxed. Getting this wrong after you stop working is expensive to fix.

- Cash flow modelling shows you a range of real outcomes, what happens if markets drop, a partner needs care, or your currency weakens. A regular retirement calculator might not be able to include all the variables.

Why Retirement Planning is Harder When You're an Expat?

Because the standard framework doesn't fit. Most retirement guides assume one country, one currency, one tax system. When your life spans borders, that assumption breaks down quickly,

The real gaps most expats could face:

- Pension pots scattered across countries - often forgotten, underperforming, or simply not reviewed since you left.

- Currency mismatch - savings in sterling or dollars, retirement spending in ringgit or baht.

- No state pension baseline - your UK state pension may be frozen, reduced or both.

- Multiple tax jurisdictions - what you owe, where, and when gets complicated fast

The longer these gaps go unaddressed, the fewer options you have to build that retirement pot.

How Much Do You Actually Need to Retire in Southeast Asia?

The 4% rule - save 25X your annual expenses is a starting point, not an answer.

For a couple living comfortably in Malaysia, private healthcare, regular travel, and a decent lifestyle, you are looking at roughly RM12,000 to RM16,000 per month in today's money. At a 4% drawdown rate, that's an investable pot of RM3.6-4.8 million, on top of any pension income.

But the number shifts based on four things regular retirement calculators typically ignore:

- Healthcare - private premiums rise sharply after 60, and some insurers stop renewing policies altogether.

- Longevity - plan to 90+, not 80+

- Local Inflation - don't use a UK or US rate on a life you're living in ringgit.

- Currency drift - a 15% move in GBP/MYR over a decade quietly reshapes your purchasing power.

Penang for example, is increasingly popular with retirees for a good reason - the cost of living, healthcare quality, and lifestyle value are hard to beat. But what "enough" actually looks like depends on where and how you want to live.

The Expat Pension Problem

Every country you’ve worked in likely left behind pension or retirement savings. Without active management, they quietly work against you, sitting in default funds, accruing charges, and subject to rules that change the moment you become a non-resident.

UK pensions — workplace, personal, and State Pension, each carry different rules around access, taxation, and transfers for non-residents, with exchange rate risk compounding the picture if you’re spending in a different currency.

US retirement accounts — 401(k)s and IRAs, can be restricted or closed by custodians once a non-US address is on file, sometimes forcing early distributions with significant tax penalties before you’re ready.

Australian superannuation is one of the most commonly overlooked assets in an expat’s financial picture, access and transfer options as a non-resident differ significantly from what most people expect.

Malaysia’s EPF now has a mandatory contribution for expats working in Malaysia, but few have factored it into their wider retirement plan, or considered what happens when they move on.

How Does Tax Residency Affect Your Retirement?

Tax becomes more complicated the moment you stop working, and for expats, it’s already complicated before that. Understanding your position before you retire, not after, is one of the most consequential things you can do.

When earned income stops, it’s replaced by pension income, investment income, and possibly rental income, each is treated differently depending on your home country’s rules and those of your country of residence. For many expats, two or more tax systems apply at once, and the interaction between them is where most surprises happen.

Key things to note:

- Tax residency vs domicile - they’re different and often misunderstood. Where you are tax resident affects how your income is taxed day-to-day. Your domicile is a separate concept, and a harder one to change. For UK nationals in particular, domicile is notoriously difficult to shift regardless of how long you have lived abroad, and it has consequences for inheritance tax and estate planning that persist even after decades overseas. If you hold nationality from another country, the rules around domicile and its estate planning implications will differ. This is an era where country-specific advice is essential.

- Double tax treaties - many countries have tax treaties with each other that determine where pension and investment income and other retirement income is taxed. Whether your home country has a treaty with your country of residence, and what it covers, directly affects, and what you receive in retirement. The specifics vary significantly between pairs, and the same type of income can be treated differently depending on which agreement applies. It is worth establishing your treaty position well before you stop working.

- Inheritance tax - not every country has one, but many do, and they interact in ways that can affect your estate from multiple directions at once. Unspent pension pots, overseas assets, and domicile status can all create tax exposure that affect your estate in ways that surprise families. It’s worth understanding how the rules interact between your home country and where you live before it becomes your family’s problem to work out. If you’re from the UK, for example, changes to inheritance tax rules from April 2027 mean pension pots are now in scope for the first time. If you have not reviewed your pension nominations and estate structure with this change in mind, it is worth doing so before that date. The broader point applies regardless of nationality: understanding how the inheritance tax rules of your home country and your country of residence interact is not an optional exercise.

What to do if you are unsure of your tax position?

The tax landscape for expats changes frequently and getting it wrong in retirement can be costly to fix. If you do not have a clear picture of your residency status, domicile position, treaty coverage, and estate exposure, speaking with an adviser who specialises in cross-border planning is the clearest path forward.

Our webinar recording on expat retirement planning covers the essentials, including tax, pensions, and cash flow modelling.

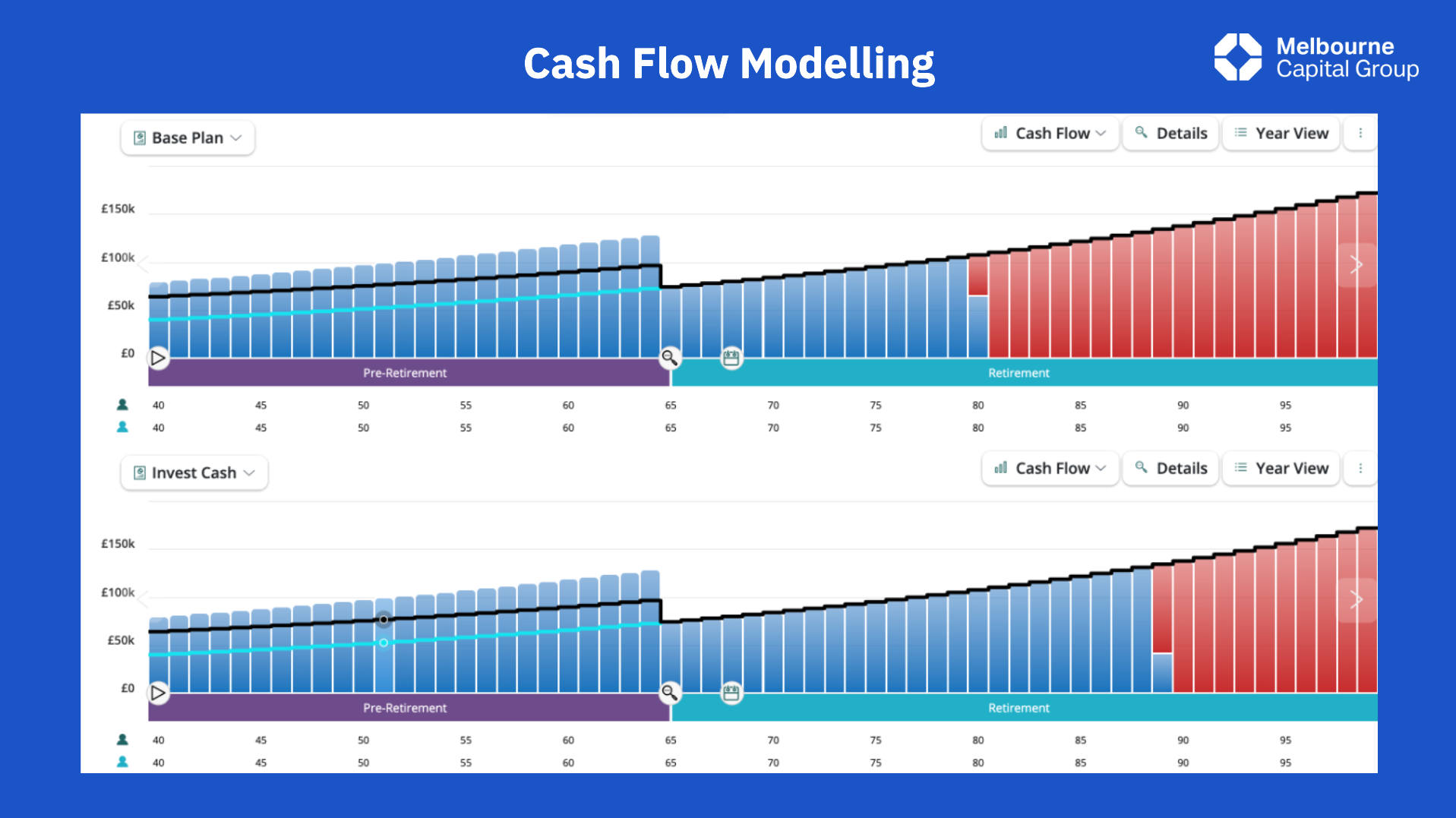

What is Cash Flow Modelling and Do You Actually Need It?

Yes, if your finances are spread across more than one country, currency or pension.

Cash flow modelling maps your financial future year by year, income in, expenditure out, assets over time, and shows you what happens under different scenarios. Not a single number. A range of outcomes.

What it answers that calculators can't:

- What does my plan look like if I retire at 55 versus 60?

- What if markets fall 30% in year two of the drawdown?

- What if one of us needs long-term care at age 76?

- What if sterling weakens against the ringgit for a decade?

For example, a British couple in KL, with two UK pensions and a USD investment portfolio, spending in ringgit, looked broadly on track under standard assumptions. The model showed two things that changed their planning: a real shortfall if one partner needed care from 76, and a meaningful drop in purchasing power under a plausible currency scenario. Six years before retirement, they had time to restructure. That is what the model is for.

Retirement calculators don't account for the expat variables that actually move the needle. Cash flow modelling does.

Are You Actually on Track? Ask Yourself These Questions

- Do you know the current value of every pension pot you've contributed to. Not approximately, but actually?

- Do you know what state or government pension entitlement you have from each country you’ve worked in, and whether gaps in your record can or should be filled?

- Do you know what tax treaty applies to your pension income in your country of residence?

- Have you modelled long-term care costs for yourself and your partner?

- Are your investments in currencies you'll actually be spending in retirement?

- Have you reviewed beneficiary nominations on your pensions? They override your will.

- Do you know what your month-one retirement income looks like, after tax and currency conversion?

If you are looking for a more structured self-audit, then our 2026 UK pension Health Check article is the best place to start.

What Should You Do Next?

If you are within five to ten years of retirement, the time to act is now, because the decisions you make in this window have the longest runway to compound.

A conversation with an adviser will help you understand where you stand.

If you'd rather start by building your knowledge, our webinar recording covers the essentials of expat retirement planning, pensions, tax, and cash flow modelling, in a way that’s practical and straightforward to follow.

Click here to access our webinar recording.

.webp)

Explore our Insights

Our team of global experts share their perspective on markets and news from the company.