EPF Contribution for Foreign Workers: What Expats in Malaysia Should Know

What is the Employees Provident Fund (EPF), and Why Should Foreign Employees Care?

As an expat or foreign employee in Malaysia, there are numerous ways to build your retirement savings, whether through diversifying investments or developing a comprehensive retirement roadmap with the help of your financial advisor.

The Employees’ Provident Fund (EPF) is Malaysia's national pension savings scheme, similar to an IRA/401K or a UK state pension. It's designed to help individuals build retirement savings through contributions from both the employer and employee. When used as part of a sound financial or investment plan, the EPF can help enhance your retirement savings.

New in 2025: Mandatory EPF Contributions for Foreign Workers

The mandate on EPF for non-Malaysians took full effect on 1st October 2025, following its initiation in March of the same year. This introduction by the Malaysian government marks a significant shift in how EPF applies to foreign workers. Previously, contributions were optional unless you were a permanent resident of the country.

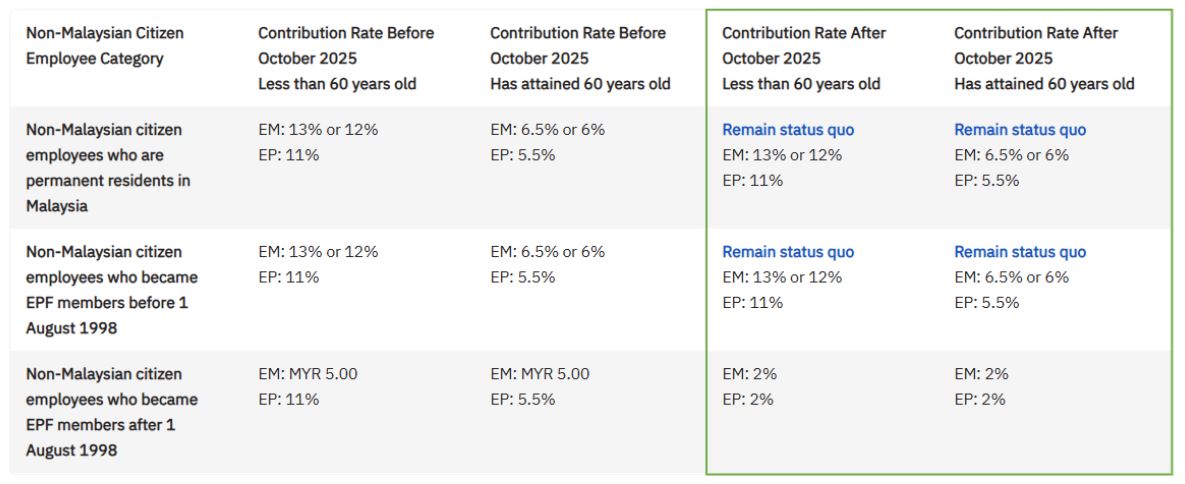

How Much is the EPF Contribution for Foreign Workers?

As of 1st October 2025, a mandatory contribution of 2% will be required from both employers and employees for non-Malaysians.

The table below outlines the specific contribution rates for different categories of non-Malaysian employees, showing the transition from previous rates to the new mandatory structure.

*EM = Employer, EP = Employee

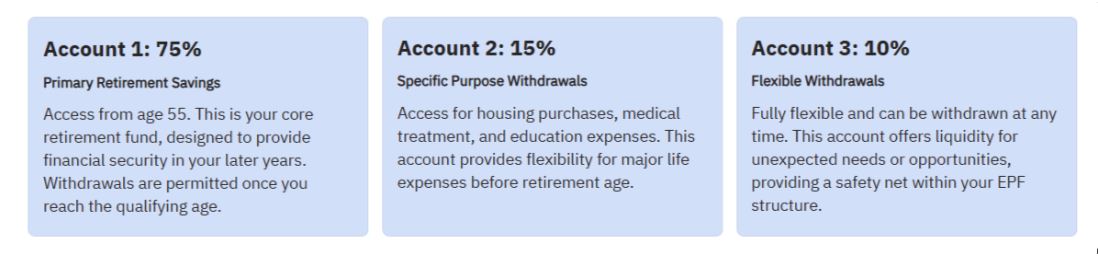

Where Does Your EPF Contribution Go?

As to how your funds are allocated in EPF, in May 2024, EPF officially restructured the way it allocates its contributions. Previously, members had two accounts, Account 1 and Account 2, where Account 1 held 70% of the contributions and Account 2 held 30%.

Now the accounts are split into three:

So, How Can I Withdraw my EPF When I Want to Return to my Home Country

It depends on your membership type.

Non-Malaysians who hold Permanent Resident status and are members registered before August 1998 will have access to all withdrawal options available, including partial withdrawals and monthly payment withdrawals.

For expats who became members after August 1998, you can only withdraw from the entire account once you have reached the age of 55. Unfortunately, there are no other withdrawal options available for expats, such as the ability to schedule a monthly withdrawal on EPF’s dividends.

Source: KWSP

More legislation and changes are scheduled for implementation in 2026, including adjustments to withdrawal guidelines for non-Malaysians, which will provide them with greater flexibility.

The Benefits of EPF for Foreign Employees in Malaysia

For expatriates working in Malaysia, the Employees Provident Fund (EPF) can be a useful vehicle for retirement savings; however, its ultimate advantage depends on your long-term plans. If you’re only here for a few years, say five to ten, increasing your EPF contributions may not always be the most strategic move. In some cases, it might make more sense to diversify or allocate funds into another currency better aligned with your future financial goals.

As Ryan Long, Private Wealth Manager at Melbourne Capital Group, noted during our webinar “What Do the EPF Changes Mean for Expats in Malaysia?”:

“If you’re a British citizen and plan to move back to the UK, we may recommend saving or investing in a currency that makes sense for you. It depends on the individual and the situation — but hedging your bets and diversifying remains the best approach.”

His advice highlights that effective planning isn’t just about where you are now, but where you plan to be next.

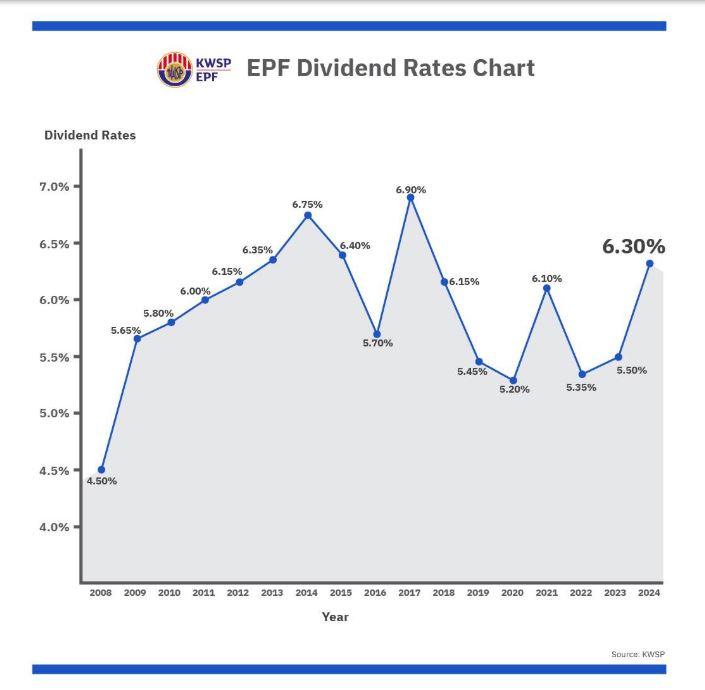

EPF “Guaranteed” Dividend Returns

By law, the EPF is required to provide a government-guaranteed minimum dividend rate of 2.5% per annum, which can be significantly higher than the rates offered by most savings accounts or fixed deposits in Malaysia. This also makes EPF a more secure investment option compared to other volatile markets. However, since 2009, the EPF has been offering average dividend rates of more than 5% per year.

Tax Savings on EPF Contributions

Contributions to EPF are tax-deductible up to a limit, which can help reduce your overall taxable income, but this applies at the annual tax relief level, not month-to-month. The tax relief for EPF contributions is capped at RM4,000 per year.

As Datin Shivajini Seelan, Chartered Accountant & Founder of JS Partners, explained during the webinar:

“Your EPF contribution isn’t tax-free on a monthly basis because your income tax is calculated on your gross salary before the deduction. So even if you increase your EPF contribution, it doesn’t reduce your overall monthly tax. What it does help with is building up your retirement savings and future gains when you eventually withdraw them — along with the tax relief that applies. But on a month-to-month basis, it’s not a direct tax reduction.”

This is a very common myth. Increasing your EPF contributions does not reduce your monthly tax, only your annual taxable income up to the RM4,000 limit.

Tax-free EPF Withdrawal for Non-Malaysian Employees

EPF withdrawals after the age of 55 are considered tax-free withdrawals, ensuring you get the most out of your retirement savings. Any withdrawals before the age of 55 from Account 2 for purposes such as medical expenses or purchasing a house are also considered tax-free withdrawals.

If you decide to leave the country permanently, the EPF allows you to withdraw all your funds in one lump sum. However, it is vital to plan your withdrawals, as you may still face income tax if you bring them back to your home country.

This is where it becomes essential to consult with a Private Wealth Manager. Our team is equipped to help you restructure your wealth to minimise tax liabilities.

Challenges of Contributing to EPF as a Foreign Employee

Despite the benefits EPF provides, there are still key challenges and drawbacks.

Currency risk is a significant challenge as the EPF fund returns are calculated in Malaysian ringgit, instead of the USD or GBP. As such, any currency fluctuations that the ringgit experiences can impact your funds and your overall purchasing power.

Another major challenge is the lack of control over the investment strategy, as EPF does not share or offer a clear view of the types of investments being made using your funds. This can severely restrict your ability to invest in higher-yield assets, as you are locked into the investments made by the EPF.

Should Foreign Workers Keep their EPF Savings or Reinvest Elsewhere?

With average dividends of around 5%, Malaysia's EPF offers stable returns, but is it the most efficient use of your savings? Some expats' EPF accounts hold over RM1 million, which could potentially be partially reinvested for greater flexibility and long-term growth.

Our Private Wealth Managers specialise in developing bespoke strategies to help you maximise your EPF funds to protect your retirement lifestyle.

That’s why we’re offering FREE access to our webinar recording on the Employees Provident Fund (EPF) framework.

Led by industry experts: Ryan Long, Private Wealth Manager at Melbourne Capital Group, who specialises in guiding expatriates through long-term, cross-border financial planning; and Datin Shivajini Seelan, Chartered Accountant and Founder of JS Partners, who advises clients on tax efficiency and corporate compliance in Malaysia.

This session will help you understand how to maximise your retirement savings while maintaining financial flexibility during your time in Malaysia.

Request now via this link.

The EPF isn't just another deduction on your pay slip. It could be a powerful part of your long-term wealth-building strategy. Get informed, plan, and make sure your savings are working for you.

If you are ready to maximise your retirement savings using EPF, schedule a one-on-one complimentary discussion with our Private Wealth Managers by contacting us.

.webp)

Explore our Insights

Our team of global experts share their perspective on markets and news from the company.

.jpg)