UK Inheritance Tax 2026/27: What Changes from 6 April and What It Means for You

.jpg)

The 2026/27 tax year brings the most significant overhaul to UK inheritance tax (IHT) in a generation. From 6 April 2026, new rules cap reliefs on business and agricultural assets, introduce a residence-based scope for non-domiciled individuals, and tighten how IHT applies to charitable legacies. For UK nationals and long-term UK residents living abroad, including many of Melbourne Capital Group's clients across Asia, these changes demand immediate attention.

This article sets out what has changed, who is affected, and what questions you should be asking.

The Core Framework: What Has Not Changed

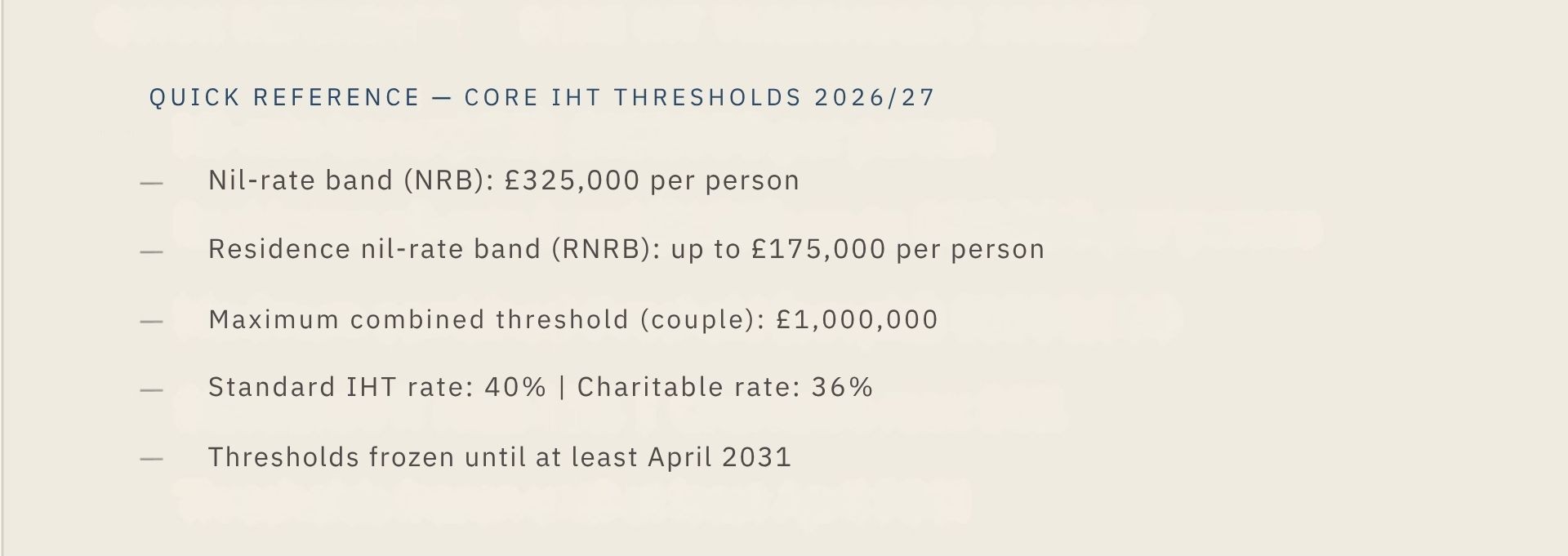

Before examining the new rules, it helps to understand what remains in place. The nil-rate band (NRB) remains frozen at £325,000 per person and is transferable between spouses and civil partners on death. The residence nil-rate band (RNRB), available when a main residence passes to a direct descendant, remains at up to £175,000 per person, though it tapers for estates above £2 million. Combined, a married couple or civil partnership can pass up to £1 million free of IHT, assuming the family home passes to children or grandchildren.

IHT continues to be charged at 40% on the taxable estate above these thresholds, or 36% where at least 10% of the net estate is left to a qualifying charity. Both the NRB and RNRB remain frozen until at least April 2031, meaning the fiscal drag of rising property and asset values will continue to pull more estates into scope each year.

The Biggest Change: Business Property Relief and Agricultural Property Relief Capped

The most significant reform from 6 April 2026 is the capping of 100% Business Property Relief (BPR) and Agricultural Property Relief (APR). Previously, these reliefs were uncapped, a qualifying family business or farm of any value could pass entirely free of IHT. That is no longer the case.

How the New Cap Works

Under Finance Act 2026, the first £2.5 million of combined qualifying BPR and APR assets per person receives 100% relief, meaning no IHT applies. Assets qualifying for these reliefs above that threshold receive only 50% relief, resulting in an effective IHT rate of 20% on the excess.

Unused allowance is transferable between spouses and civil partners on death, in the same way as the NRB. This means a couple may together shelter up to £5 million of qualifying business or agricultural assets from IHT entirely.

What Qualifies and What Does Not

Property that continues to qualify for 100% relief (up to the £2.5 million allowance) includes agricultural land, farm buildings and farmhouses, and trading businesses. Shares listed on markets not meeting HMRC's definition of 'listed', including the Alternative Investment Market (AIM), are restricted to 50% relief regardless of value and do not count against the £2.5 million allowance.

For those holding multiple qualifying assets, HMRC's new apportionment tool (published 6 April 2026) must be used to calculate how the £2.5 million allowance is divided across the estate. The allowance must be proportionally allocated, it cannot be directed entirely to a single asset.

Non-UK Structures Holding UK Agricultural Land

A further technical change brings agricultural property held through non-UK incorporated companies or trusts into the scope of UK IHT. Previously, certain offshore structures could hold UK farmland outside IHT reach. Those arrangements no longer provide that protection from 6 April 2026.

Gifts Made After 30 October 2024

Gifts of qualifying business or agricultural property made on or after 30 October 2024 count against the £2.5 million allowance if the donor dies within seven years. This anti-forestalling measure means that those who gave away assets before April 2026 in anticipation of the changes may still find the relief capped if they die within the seven-year window.

Paying the Tax: The Ten-Year Instalment Option

For illiquid assets such as businesses and farms, where a significant cash liability could force an immediate sale, estates may elect to pay the IHT due on those assets in equal annual instalments over ten years, interest-free. This option, available from April 2026, provides breathing room for families who need time to raise funds without disposing of the underlying asset.

Estates should nonetheless plan ahead for how a liability will be met, whether through business reserves, insurance, trust structures, or phased succession, since a ten-year obligation still requires careful management.

How the Changes Affect Non-Domiciled Individuals

For anyone who is non-UK domiciled or have left the UK, the 2026/27 changes interact with a broader reform that came into effect a year earlier, the shift from a domicile-based to a residence-based IHT system, effective from 6 April 2025. Understanding both sets of rules together is essential.

The New Residence-Based Scope

Under the pre-2025 rules, non-UK domiciled individuals were only subject to UK IHT on UK-sited assets. From 6 April 2025, this changed: non-UK assets are now within the scope of UK IHT if the individual qualifies as a 'long-term resident', defined as being UK tax resident in 10 or more of the previous 20 tax years. The previous threshold was 15 of 20 years.

UK assets continue to be within IHT scope at all times, regardless of domicile or residence status.

The Tail: Continuing Exposure After Leaving the UK

Long-term residents who leave the UK remain exposed to IHT on worldwide assets for between 3 and 10 years depending on their prior period of UK residence. Those with 20 or more years of UK residence face a ten-year tail. Individuals who left the UK before 6 April 2025 and did not return benefit from transitional rules, retaining the prior three-year tail.

Excluded Property Trusts

Excluded property trusts, structures in which non-UK assets are settled by a non-domiciled individual, historically provided significant IHT protection. From April 2025, if the settlor is a long-term resident at the time of a chargeable event, the trust's non-UK assets are no longer excluded from IHT. Transitional protection exists for trusts settled before 30 October 2024.

Application of the BPR/APR Cap to Non-Doms

The new BPR and APR relief cap applies equally to non-domiciled individuals in respect of UK assets: there is no special treatment. For non-doms who have become long-term residents and hold qualifying business or agricultural assets outside the UK, those assets are now both within IHT scope and subject to the same relief cap.

Charitable Legacies: A Tightening of Qualification

A less-discussed change also takes effect from 6 April 2026. To qualify for IHT relief, charitable gifts in a will must now be made directly to UK-registered charities or eligible amateur sports clubs. It is no longer possible to leave assets to trustees with instructions to apply them to charitable purposes at a later stage, a mechanism that in some cases had been used to benefit non-UK charities or less clearly regulated bodies.

For anyone with philanthropic intentions as part of their estate plan, this change requires a review of existing wills.

.jpg)

What This Means for UK Nationals and Those with UK Ties Living in Asia

Melbourne Capital Group works with internationally mobile clients across Asia; UK nationals and dual-nationals living in Malaysia, Thailand, the Philippines, Saudi and beyond. Some have left the UK recently; others have been away for decades. Some plan to return; others do not. Many still hold UK property, business interests, pension assets, or family trusts. What all of them share is a continuing connection to a UK tax system that has just become significantly more complex.

These reforms are not only relevant to those with large business or agricultural estates. The interaction of frozen thresholds, rising UK asset values, the new residence-based scope for non-doms, and the tightening of relief caps means that estates of more modest size, particularly those combining UK property with overseas savings or investments, can now cross meaningful IHT thresholds.

Five Actions to Take Now

1. Establish your residency position.

Count the number of tax years you have been UK resident in the past 20. If the total is ten or more, you are likely a long-term resident and your worldwide assets may be within UK IHT scope. If you left the UK having been resident for 20 or more years, you face a ten-year tail, meaning IHT exposure on global assets continues for a decade after departure. This calculation is the foundation for everything else.

2. Review your UK asset picture.

Take stock of everything you hold in the UK: property, business interests, investments, pension assets, and jointly held assets. Understand their current value and consider how they interact with the NRB, RNRB, and where applicable, the new £2.5 million BPR/APR cap. Many clients who have not reviewed their UK estate position for several years will find the picture has changed materially.

3. Check your will, particularly any charitable provisions.

If your will has not been updated since October 2024, it may need to be. The new rules around charitable legacies require gifts to be made directly to UK-registered charities. Any instruction leaving assets to trustees for later application to charitable purposes may no longer qualify for IHT relief. A will review is a straightforward step and one that can prevent significant unintended tax consequences.

4. Assess any trust arrangements.

If you settled assets into an excluded property trust while non-domiciled, and you have since become a long-term resident, the protection that structure provided has changed. Pre-October 2024 trusts benefit from some transitional relief, but the position requires specialist review. Do not assume existing structures remain effective without taking advice.

5. Plan for liquidity not just liability.

Even where the IHT liability itself is understood, many estates lack the liquidity to pay it. This is particularly acute where the estate includes illiquid UK property or business assets. Conversations about how a future liability would actually be funded, whether through insurance, structured gifting, business reserves, or the new ten-year instalment option, are as important as calculating what the liability is.

Next Steps

These changes are now in force. If any of the following apply to you, this is the right time to seek professional advice:

- You hold, or expect to inherit, a family business or agricultural property in the UK with combined qualifying value above £2.5 million.

- You are a UK national who has been resident in the UK for a total of ten or more years in the past twenty, whether continuously or otherwise.

- You hold assets in excluded property trusts or offshore structures linked to UK agricultural land.

- Your will includes charitable gifts or directions to trustees regarding charitable purposes.

- You are planning to return to the UK, or are uncertain whether your current residence pattern crosses the long-term residency threshold.

Melbourne Capital Group's role is to work alongside qualified UK tax advisers and estate planning specialists to ensure your overall financial plan reflects the full picture, not just your investment portfolio, but how your assets will be structured, protected, and passed on. These conversations are most valuable when they take place before decisions are made, not after.

Sources:

- RSM UK – Inheritance Tax Changes: Key Facts to Know Before the April 2026 Deadline https://www.rsmuk.com/insights/tax-voice/inheritance-tax-changes-key-facts-to-know-before-the-april-2026-deadline

- Chartered Institute of Taxation – New Tax Year, New Rules: What's Changing This April https://www.tax.org.uk/new-tax-year-new-rules-what-s-changing-this-april

- GOV.UK / HMRC – Work Out How to Apportion Agricultural and Business Relief for Inheritance Tax https://www.gov.uk/guidance/work-out-how-to-apportion-agricultural-and-business-relief-for-inheritance-tax

Supporting regulatory references:

- GOV.UK – Business Relief for Inheritance Tax https://www.gov.uk/business-relief-inheritance-tax

- GOV.UK – Agricultural Relief on Inheritance Tax https://www.gov.uk/guidance/agricultural-relief-on-inheritance-tax

- GOV.UK / Finance Act 2026 – Inheritance Tax: Reforms to Agricultural Property Relief and Business Property Relief https://www.gov.uk/government/publications/inheritance-tax-reforms-to-agricultural-property-relief-and-business-property-relief

- HMRC – HMRC Apportionment Tool for APR/BPR https://www.tax.service.gov.uk/guidance/Check-how-to-apportion-Agricultural-and-Business-Property-relief-for-Inheritance-Tax

Important Information

This article is intended for general information purposes only and does not constitute financial, tax, or legal advice. The information reflects legislation and HMRC guidance in force as at 6 April 2026 and is subject to change. Melbourne Capital Group does not provide UK tax advice. You should seek independent advice from a qualified UK tax adviser and legal professional before making any decisions in relation to your estate plan. Past performance is not indicative of future results.

.webp)

Explore our Insights

Our team of global experts share their perspective on markets and news from the company.

.jpg)