Financial health checks: a vital first step for expats seeking a secure financial future

Jake Mowson, Private Wealth Manager, explains what a financial health check involves and why it matters for expats managing cross-border finances to foster long-term wealth.

In my experience, most people want a financially secure future, but when asked, few can provide a concrete explanation as to how they intend to achieve it. This is where financial planning comes in.

A good financial plan can provide a clear pathway, helping someone build wealth and achieve their financial goals. However, the ability to create and execute a plan is entirely predicated on first understanding that person’s current financial situation.

Think about it in terms of going on a journey; they may have a destination in mind, but unless they know their starting point, a map is going to be useless. It's this 'starting point' that a financial health check seeks to establish.

Key takeaways

In this article, I will explain;

- How a financial health check reviews your income, savings, assets, investments, pensions, insurance, and debt to create a full picture of your current financial position.

- Why a financial health check matters more for expats who have unique complexity due to fragmented assets across borders, dealing with multiple currencies, and reduced access to state-backed safety nets.

- how cash-flow analysis and clear goal setting are core components of an effective check.

- Why starting early matters. Compounding rewards time in the market more than timing it.

- The value of reviewing. That a financial health check is not a standalone exercise and one that should be revisited after major life changes.

What is a financial health check?

A financial health check is a review of an individual's finances in their entirety. It will look at income, savings, assets, investments, pensions, insurance, debt and any/all other obligations. The purpose of the exercise is to create a detailed snapshot of that individual’s specific financial situation, providing clarity and understanding about where they are now. It will also reveal strengths and, crucially, weaknesses.

In my experience, weaknesses identified during a health check are rarely known about or understood prior. This isn’t necessarily because the person doesn’t have a handle on their finances per se, but because they aren’t particularly obvious. For instance, it could be that an individual is far more financially vulnerable in a crisis than they were aware of due to inadequate personal protection. Or they might have a long-abandoned pension that’s no longer working to support their interests. Whatever the issues may be, tackling them is only possible once they are known.

Why is a financial health check especially important for expats?

We all have increasingly fragmented financial lives. It’s not uncommon for someone to have multiple accounts and investments spread across various platforms, and while this approach can add value and promote diversification, it makes it harder to see the complete financial picture. This is even more true of expats whose wealth is likely to be both fragmented and span borders, something I understand personally, having lived as an expat in Malaysia for almost a decade while raising my family with my Malaysian wife.

It’s commonplace for an expat to hold pensions, properties, savings and investments in multiple countries. It’s also more likely for their income and obligations to be different currencies, opening them to currency fluctuation related risk. In addition, they may still have tax reporting obligations in their home country. Given all these variables, it makes creating that full financial picture more challenging but also more necessary.

Expats, by virtue of not being a citizen in the country in which they are living, are unlikely to have the same access to financial support mechanisms that a citizen may have. For instance, a state-backed retirement fund or healthcare, housing or education schemes. This puts the onus for financial security firmly on the individual and makes long-term financial planning more pressing.

What is cash-flow analysis and what role does it play in a financial health check?

Cash flow analysis is the process of examining income and expenses over a specific period. It involves identifying income sources such as salary, investments, or side businesses and compares them against expenses including housing, utilities, groceries, debt repayments, insurance, and discretionary spending.

A positive cash flow is when income exceeds expenses. This surplus can then be allocated to savings, investments, debt reduction, or emergency funds. A negative cash flow indicates that spending is greater than income and may highlight the need for budgeting adjustments or debt management strategies.

As part of a financial health check, cash flow modelling can also help identify potential shortfalls before they occur, effectively stress-testing an individual's current financial situation. It can also seek to determine whether current savings levels are sufficient and evaluate the impact of major financial decisions. It can also be used to test “what-if” scenarios such as early retirement, purchasing property, taking a career break, or increasing investment contributions. This allows individuals to understand the financial consequences of different choices in a risk-free environment and make more informed decisions.

Ultimately, a cash-flow analysis helps an individual understand where their money is currently going with a view to identifying where it might be better spent or invested.

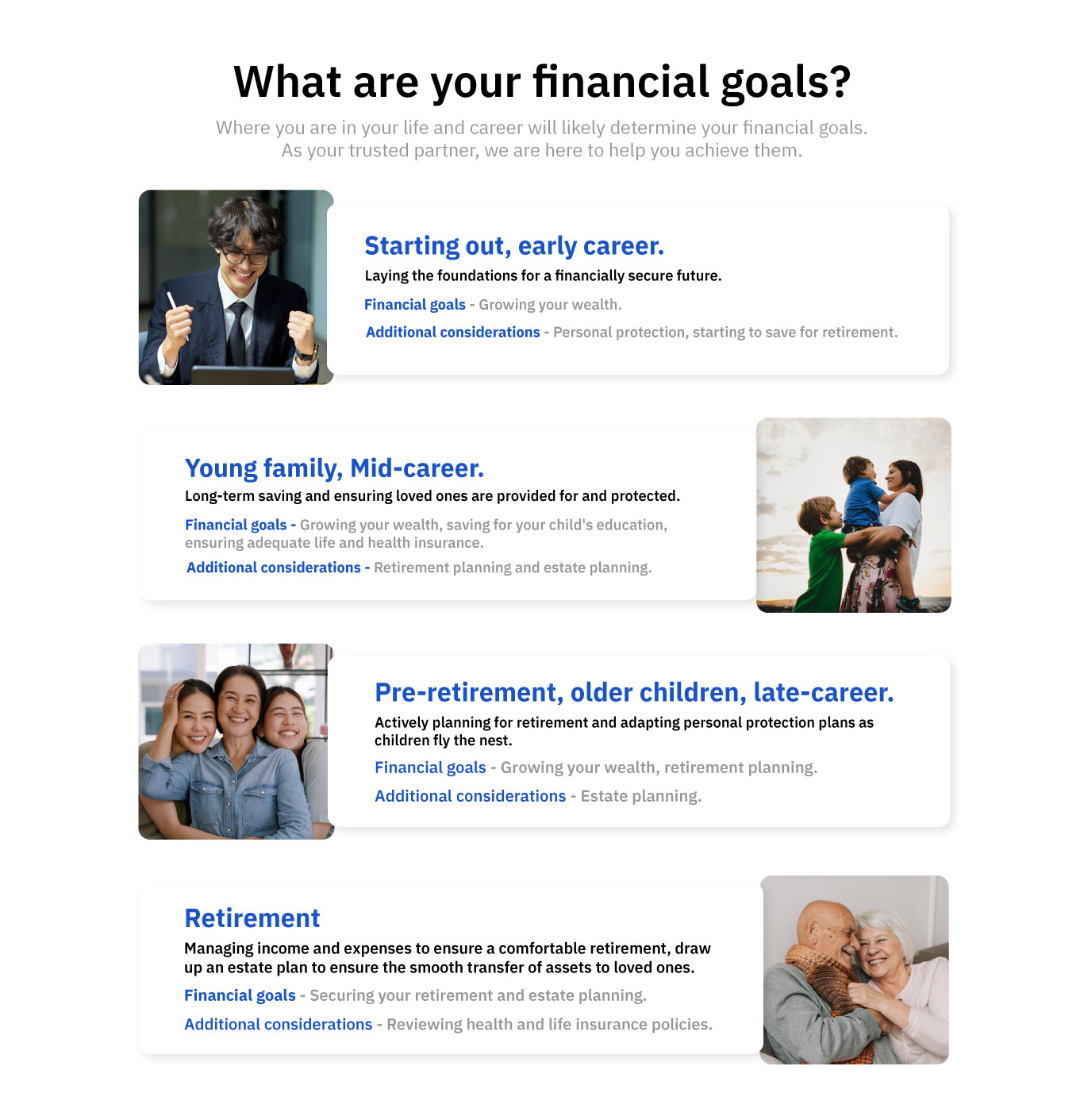

Identifying financial goals and priorities.

Effective financial planning is not just about managing money today. It is about ensuring your financial decisions support the life you want in the future. So, an important part of a financial health check is understanding what the end goals are. Is it building a retirement fund? Putting a child through university? Purchasing a property? Part of establishing a goal is also setting them in the context of a timeline. So, when does the child go to university? When does the person want to retire?

Having short-, medium- and long-term objectives helps to prioritise saving and investment strategies. Informing where the money identified in during the cash-flow analysis would be best directed.

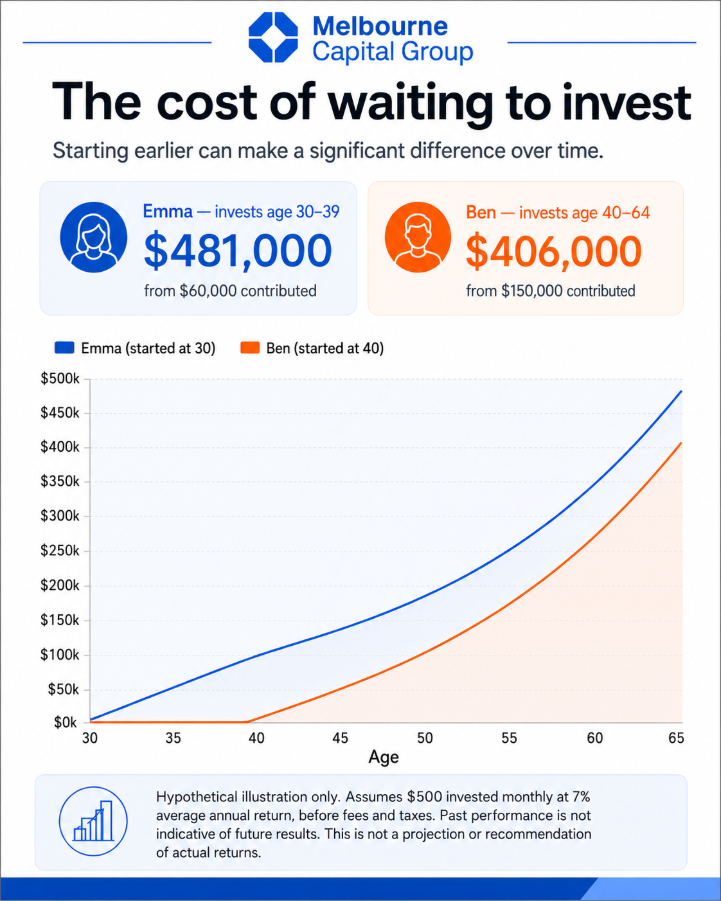

Why starting early matters; the power of compounding.

It’s tempting to put off a financial health check much as it to put off a visit to the doctor or a dentist. Most people recognise they should make a financial plan, but anxiety can get in the way perhaps worrying that their financial goals are unachievable. Paradoxically, the longer they put off financial planning, the more likely it is for their financial goals to become more challenging. This brings me to perhaps one of the most powerful wealth-building principles in financial planning; compounding.

Put simply, compounding occurs when the returns generated by investments begin to generate returns of their own, creating a snowball effect over time. This means that even relatively modest but consistent contributions can grow into substantial wealth when given enough time. As Warren Buffet famously put it; time in the market beats timing the market.

A financial health check helps identify opportunities where an individual can start investing sooner, maximising any available surplus income, and ensuring money is working efficiently towards a person’s objectives.

To offer an example; someone who begins investing regularly in their thirties may accumulate significantly more wealth than someone who delays until their forties, even if the latter invests larger amounts.

Why regular financial health checks matter?

A financial health check should not be viewed as a one-off exercise. Circumstances change and a financial strategy needs to evolve with the person to reflect changing priorities, opportunities and challenges. Whether those changes involve a promotion, relocation or the birth of a child; regular reviews allow the opportunity to reassess whether a current wealth management strategy is still aligned with the life that person is living now and the future they’re aiming for.

Building long-term financial security as an expat

For expats managing cross-border finances, a regular financial health check is one of the most effective ways to bring clarity, confidence and control to long-term financial planning. By reviewing savings, investments, pensions, protection, cash flow and future goals in one place, internationally mobile individuals can identify risks, uncover opportunities and make more informed decisions about their wealth. To have a bright financial tomorrow, it’s important to understand where you are today.

Here at Melbourne Capital Group we fully understand that everyone’s goals, timeframe and capacity to save are different, and there is no such thing as one size fits all. We are committed to assessing every person individually and taking time to understand their individual circumstances. If you have a financial goal that you need to reach, no matter how big or small, then feel free to get in touch to discuss how we can help with the guidance and discipline to support you in your endeavours.

Jake Mowson is an experienced financial planner with a long history of guiding internationally mobile clients through their financial journey and providing them with the blueprints they need based on their goals. Please don’t hesitate to contact him at jakemowson@melbournecapitalgroup.com or connect with him on Linkedin.

Please note this is not financial advice and should not be construed as such.

.webp)

Explore our Insights

Our team of global experts share their perspective on markets and news from the company.

.jpg)