Islamic and Halal Investing: Ethical Investment Strategies for the Modern World

.jpg)

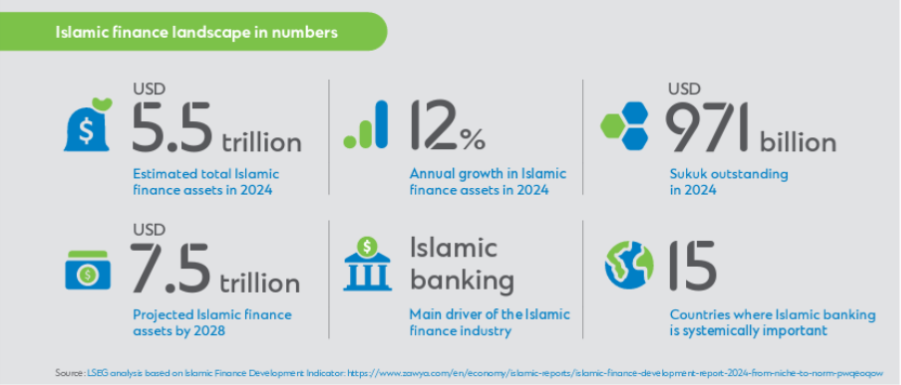

Islamic finance, once categorised as a niche alternative to conventional finance, has today incorporated itself to be a globally recognised segment of the financial industry. Reaching USD5.5 trillion in global assets in 2024, the growth within this space has been remarkable, this is a 12% rise from 2023 and a 43% increase from 2020. Standard Chartered have projected Islamic Finance to surpass USD7.5 trillion by 2028*. Though still a fraction of the total value of global financial assets, this growth should not go unnoticed.

What is Islamic Finance and Halal Investing?

Islamic finance is a system of financial activities governed by Shariah (Islamic law), which prohibits riba (interest) and gharar (uncertainty), and promotes ethical, asset-backed transactions. Halal investing applies these principles to investment decisions, ensuring that capital is placed only in ventures and companies whose activities are permissible under Islamic law. This includes avoiding industries like alcohol, gambling, tobacco, and other harmful sectors, while encouraging investments that support real economic activity and societal benefit. By focusing on transparency, risk-sharing, and tangible assets, Islamic finance and halal investing aim to generate sustainable returens without compromising religious values.

Difference between Shariah-Compliant Sukuk vs. Conventional Bonds

Without getting too complicated, conventional bonds are considerd non-Shariah compliant because their returns are based on “interest”. Instead, Islamic Finance offers Sukuk which at its core has a similar objective as a bond, and is structured in a way that investors are given partial ownership of the asset, project or anything related to the needs of issuing the Sukuk. Returns are derived from the profit-sharing or rental income, having said that, as with bonds, this carries a risk of a company or issuer facing difficulties, in this case, the Sukuk holder may not receive their principal in full.

During the 2008 Global Financial Crisis, Sukuk suffered similar declines to conventional bonds. However, further scrutiny revealed that the sell-off was driven more by market sentiment than the underlying investment structure. Thanks to being asset-backed and having no exposure to leverage, Sukuk recovered more quickly post-crisis. This resilience increased awareness and demand, improving liquidity in the years that followed.

The Rise of Sukuk and Green Sukuk as Halal Investment Options

In 2024, total Sukuk issuance was approximately USD180 billion and is on track to surpass USD1 trillion in outstanding issuance in the next few years*. While Malaysia once held nearly 70% of the market share in 2007, Saudi Arabia and Indonesia have since taken the lead. Malaysia remains an important innovator, introducing innovative structures, such as the Green Sukuk, a Shariah-compliant investment certificate specifically designed to raise capital for environmentally sustainable projects. Since then, “Green Sukuk” now represents 10% of the overall Sukuk market.

Benefits and Risks of Halal Investing

Halal investing offers several benefits, including alignment with ethical and socially responsible values, diversification through access to Shariah-compliant global markets, and potential resilience in times of financial stress due to its emphasis on asset-backed structures and low leverage. Many Muslim investors also appreciate the transparency in screening processes, knowing their capital avoids industries considered harmful.

However, halal investing also carries risks. Shariah-compliant portfolios may have a smaller investable universe, which can limit exposure to certain high-growth sectors. Additionally, while asset-backed structures like Sukuk can offer stability, they are not immune to market volatility or issuer default risk. Investors must also consider currency fluctuations, regulatory differences between jurisdictions, and the possibility that interpretations of Shariah compliance can vary, affecting investment eligibility.

ESG Investing and Its Parallels with Islamic Finance

The increasing global demand for Environmental, Social, and Governance (ESG) investment has also boosted interest in Shariah-compliant investments due to their similarities. Both approaches prioritise ethical considerations and responsible behaviour. Fund managers screening for compatibility of the companies often focus on the same matter, such as activities that have a negative societal impact mentioned before, like tobacco, alcohol and gambling and environmentally harmful activities promoting responsible resource management.

Though some text may highlight that investors' choices may be limited should they require a Shariah-compliant portfolio, as this no longer holds ground. The chart below is not meant to highlight the performance but rather to emphasise that the 500 largest companies which are Shariah-compliant listed in the US can produce returns on a similar trend.

Source: SP Global

Shariah Investment Screening Criteria and Flexibility

Some facts to note are that there is flexibility when it comes to screening a company if they are Shariah-compliant. For example, a company’s revenue from “haram” activities should not exceed a 5% threshold, its debts and any interest (riba) bearing assets should not exceed one-third of its total assets, and non-compliant income (e.g. riba) should not exceed 5%.

Most times, an index or a fund which is certified as Shariah-compliant is first validated by an Islamic Scholar, who takes a pragmatic approach to screening. Whilst the objective is to make sure the company upholds Islamic principles, the scholars recognise the complexity of on-the-ground business models and the need for reasonable flexibility. For example, in Malaysia the Shariah Advisory Councils (SAC), which consists of Islamic Scholars, oversee and advise the Securities Commission on Islamic-related queries, and issues fatwa (non-binding religious opinions) on compliance.

To encourage Muslim participation in global markets encourage halal wealth creation and avoid hardship or exclusion from economic progress, thresholds have in some cases been raised, for example, from 5% to 20% for certain activities. Most Islamic scholars apply the principles of Mashalah (public benefit) and Urf (custom) when it comes to screening these companies. Businesses have also contributed to the rise in Shariah-compliant investments in a similar way they are trying to be ESG-compliant to attract the millennials and Gen Z’s.

Why Halal Investing is Becoming a Mainstream Strategy

With every aspect aligned, the concept of Islamic investments will no longer be something that impacts the portfolio in terms of diversification, but a sought-after exposure in a portfolio mirroring the demand for ESG investments.

Suresh Raj, Private Wealth Manager, is a shariah-certified financial adviser based in Malaysia. He brings over a decade of expertise in high-net-worth portfolio management. From his start during the 2008 crisis to managing portfolios in Malaysia and Singapore, Suresh remains committed to client-focused, goals-based financial planning at Melbourne Capital Group. Connect with him on Linkedin or email him at sureshraj@melbournecapitalgroup.com for more information.

References:

- Standard Chartered: Global Islamic Finance Assets to Surpass USD 7.5 trillion by 2028.

.webp)

Explore our Insights

Our team of global experts share their perspective on markets and news from the company.

.jpg)