How to Choose between International Health Insurance or Caisse des Français de l’Étranger (CFE)

.jpg)

Moving abroad often means navigating layers of life administrative changes, and healthcare is one of the biggest considerations. Whether you're planning a short-term assignment or a permanent move, understanding the differences between CFE and international health insurance can save you thousands of euros, and give you peace of mind when you need it the most.

When I discuss health coverage with my clients, some tell me they are already insured through the Caisse des Français de l’Étranger (CFE). For those unfamiliar with this organisation, perhaps because they are not French or not yet expatriates, it is worth explaining what the CFE is and how it compares to an international health insurance policy.

What is the Caisse des Français de l’Étranger (CFE)?

The CFE is a French social security body dedicated to expatriates. It enables French citizens living abroad to maintain a “Sécurité sociale”-type health coverage, even if they are no longer affiliated to the French general system.

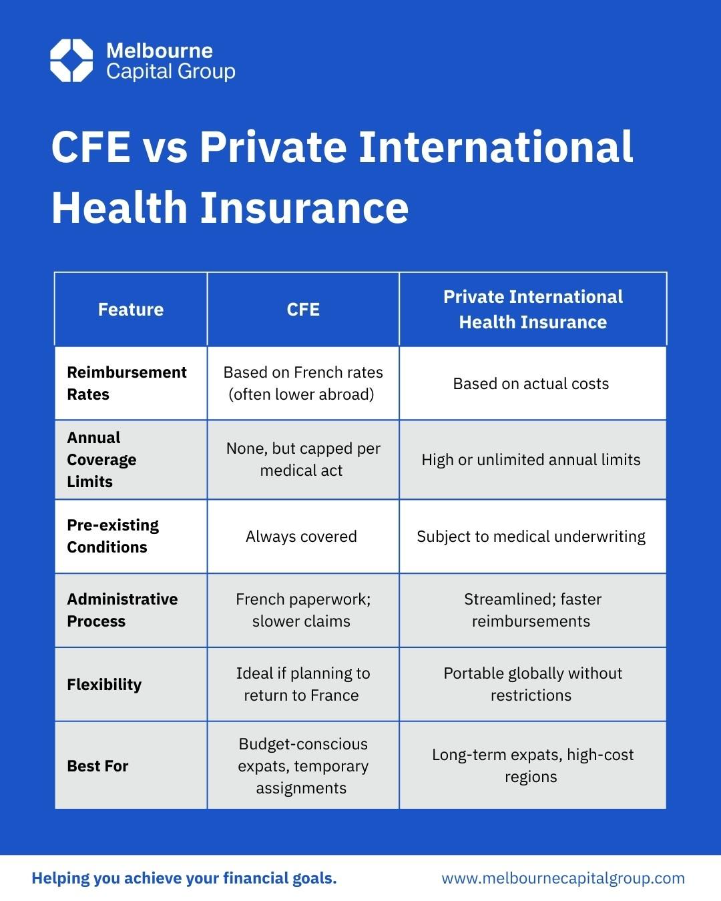

While it replicates the benefits of the French social security system for those residing abroad, reimbursements are calculated based on French rates, which are often lower than actual healthcare costs outside Europe.

Membership is available at any time, even after several years spent abroad.

CFE Coverage Options

The CFE offers three main categories of coverage:

- Illness, maternity, disability

- Workplace accidents and occupational diseases

- Pension contributions: an option to continue contributing to the French state pension system

How Much Does the CFE Cost?

The CFE premiums are calculated based on:

- Age

- The chosen plan (solo or family contract)

For example, someone aged between 45 and 59 would pay around €124 per month (about €1,488 per year) for illness and maternity coverage alone.

If you join within three months of leaving France, there is no waiting period: your cover begins immediately. After that, the waiting period may be up to six months for illnesses (none for accidents).

Key Advantages of the CFE

- No medical questionnaire required for enrolment

- Worldwide coverage, including temporary stays in France

- Cover for pre-existing medical conditions

- Immediate reinstatement into the French social security system upon permanent return

CFE Healthcare Reimbursements

Although the CFE provides global coverage, reimbursements are based on French rates and can be far lower than actual medical expenses abroad.

Examples in Malaysia (private healthcare):

%201.JPG)

Without supplementary insurance, a single hospital stay can leave you with a significant financial burden.

CFE vs Private International Health Insurance

Example Expat Scenarios

- Young Single in Thailand: Low healthcare needs and a limited budget - CFE alone may be enough.

- Family in Saudi Arabia: High-cost city and family healthcare needs - CFE with supplementary cover or a private plan is almost always necessary.

- Retiree in Malaysia: Planning to stay long-term - a standalone private health insurance plan with higher limits and simpler administration often provides better value.

CFE + Supplementary or Standalone Health Insurance?

Many expatriates opt for a mixed solution:

- CFE as a base

- An international health insurance policy to cover the shortfall

However, combining CFE contributions with a supplementary policy can, over the long term, cost as much – or even more – than a 100% private international policy.The difference is that private cover usually applies a global annual limit (often very high), rather than a limit per medical act.

A private health insurance policy, however, generally offers:

- Higher reimbursement ceilings

- Simpler administration

- Reimbursement based on actual costs

Over a ten-year period, the total cost of CFE + supplementary cover and that of a standalone health insurance policy work out to be similar.

How Should Expats Decide Between Caisse des Français de l’Étranger or International Health Insurance?

Ask yourself these key questions:

- What country are you living in, and how expensive is healthcare there?

- Do you have any pre-existing conditions?

- How long do you plan to live abroad?

- Are you likely to return to France in the future?

- Is having cashless hospital access a priority for you?

When to Favour the CFE?

Other Considerations for French Expats

- Integration with local systems: In some countries, CFE can complement local health schemes

- Portability: Private health insurance often allows seamless transitions between countries

- Tax efficiency: Depending on your country of residence, certain health-related contributions may or may not be deductible. Always consult a qualified tax advisor to understand how CFE contributions are treated in your jurisdiction.

Conclusion

Every situation is unique. Whether you are already covered by the CFE with supplementary insurance or by a standalone international health policy, it is essential to regularly review your cover to ensure it remains aligned with your needs, your budget, and your priorities.

Contact me at xavierblaise@melbournecapitalgroup.com to review your situation together and determine the best health cover strategy for living abroad.

Xavier is a Belgian expatriate who has called Malaysia home for nine years. After the COVID years sparked a shift in his professional aspirations, he transitioned in 2022 as a licensed Financial Adviser at an offshore investment firm. Leveraging his experience and deep understanding of the financial services landscape, Xavier now helps fellow expats and locals invest securely, whether it’s to fund life projects, plan for children’s education abroad, or build a comfortable retirement. Connect with him on Linkedin.

.webp)

Explore our Insights

Our team of global experts share their perspective on markets and news from the company.